Credit scores are a necessary factor in accessing loans and other forms of financing, while reducing debt allows individuals to increase their net worth. The article discusses strategies to create credit and pay off debt so readers can decide how best to manage their finances and achieve a positive impact.

Creating credit involves getting loans or using a line of credit to establish a history with creditors. Good payment habits lead to higher credit scores, allowing people to access more money when needed. Therefore it is necessary to understand how different types of accounts affect one’s score, what constitutes good payment practices, and how this will positively impact their financial situation.

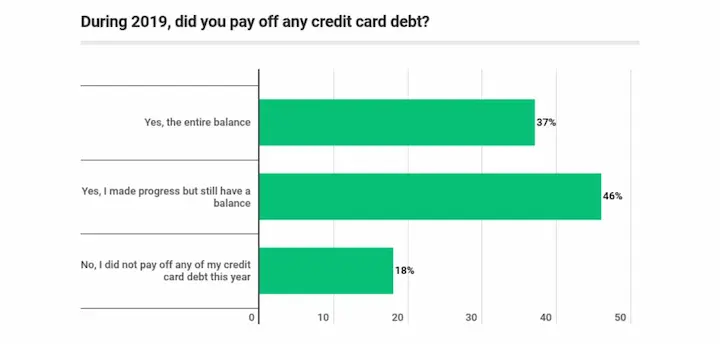

Paying off debt helps build overall wealth by freeing up income that otherwise goes toward loans or lines of credit payments. It is beneficial because it reduces interest rate charges, allowing more money to remain in savings instead of going towards extra costs associated with carrying a balance on an account. Strategies such as budgeting, reducing expenses, and utilizing lower-interest loan options must all be considered when attempting to pay down debts quickly and efficiently.

What is Upgrade Personal Loans?

Upgrade personal loans allow borrowers to save money by combining certain debts into one loan with lower interest rates or extended payment terms. It gives borrowers extra funds for other expenses such as home improvements or consolidating higher interest rate cards. You can establish good credit history through regular payments and improve your overall credit score over time by using the extra cash wisely. It helps you build up your financial security even further.

The table summarizes the different features and requirements of Upgrade personal loans according to Nerdwallet.

| Feature/Requirement | Description |

|---|---|

| Minimum Credit Score | 560 (FICO score version 9 from TransUnion) |

| APR | 8.24% – 35.97% |

| Fees | Origination: 1.85% – 8.99%, Late fee: $10, Failed payment fee: $10 |

| Loan Amount | $1,000 – $50,000 |

| Repayment Terms | 2 – 5 years; 7 years for home improvement loans and loans over $30,000 |

| Time to Fund After Approval | One day |

| Multiple Rate Discounts | Autopay discount of 0.5%, Direct pay discount of 1% – 5%, Rewards checking discount of up to 20% |

| Charges Origination Fee | 1.85% – 8% origination fee |

| Minimum Number of Accounts on Credit History | One account |

| Minimum Length of Credit History | Two years |

| Maximum Debt-to-Income Ratio | 75%, including the mortgage and the loan being applied for |

| Average Credit Score of Borrower | 672 |

| Average Annual Income of Borrower | $80,000 |

| Average Loan Amount | $10,100 |

| Average Loan Term | Five years |

Upgrade Personal Loan Features and Requirements

The table provides a comprehensive overview of Upgrade personal loans, making it easier for borrowers to compare and decide if Upgrade is the right lender. It includes the minimum requirements to qualify for a loan, the average credit score, annual income, loan amount, loan term of a borrower, and the most common loan purpose. The table includes the minimum credit score required, the APR range, fees, loan amount, repayment terms, time to fund after approval, loan availability, and discount rates.

Using upgraded personal loans effectively takes research and strategizing. Still, it proves beneficial when looking to create credit and pay off the debt efficiently, ultimately leading to debt freedom. Lenders want assurance that their customers will fulfill their financial obligations, so making wise choices now help set yourself up for success.

Benefits Of Upgrade Personal Loans

Upgraded personal loans provide practical solutions which help improve financial security. Upgrade personal loans offer certain advantages that benefit individuals looking to free themselves from the burden of their current debt obligations and work towards debt freedom. Listed below are the benefits of upgraded personal loans.

- Flexible payment options – Upgrade personal loans give borrowers more lenient repayment options when compared to traditional forms of credit, such as credit unions. It means you have lower monthly payments or longer terms available if needed.

- Low interest – Borrowers can benefit from low-interest rates and fees with upgraded personal loans, saving them money in the long run, even when compared to credit unions.

- Reports to three major bureaus – A bonus is that upgrade personal loan accounts are reported to all three major credit bureaus, helping build or rebuild your credit score over time, just like traditional credit unions.

The benefits make it clear why many people turn to this financing option to manage their debts responsibly while still having access to necessary funds when needed. Finding an affordable solution has always been challenging due to lenders offering competitive rates on such products, including online lenders and traditional credit unions.

Annual Percentage Rate (APR)

The APR accurately summarizes the interest rate on one’s loan by considering other costs associated with obtaining credit, such as processing fees and commission charges. It expresses the costs in yearly percentage rates so consumers can compare different loans more easily. The metric allows borrowers to gain greater transparency when assessing their financial options, including all extra expenses related to borrowing money. Understanding the APR helps them decide how much they will pay back over time, allowing them to budget accordingly and reduce potential financial risks.

Home Renovations Financing With Upgrade Personal Loans

Upgrade Personal Loans provide competitive Annual Percentage Rates (APR). It allows borrowers to take advantage of the low cost of borrowing money without sacrificing quality or service. Upgraded personal loans help individuals build a credit history by allowing them to manage debt responsibly. The flexible repayment options make it easy for borrowers to tailor their payments to meet their budget needs and preferences. The application process is simple, which helps guarantee that applicants get approved quickly.

An upgraded personal loan is ideal for people seeking to renovate their homes but has limited resources available for the project. Homeowners can access funds in just a few days and make improvements immediately. They can rest assured that they’re getting the best rates on the market and friendly customer service when needed. All combine into one convenient package: fast approval, affordable APR, and excellent customer support creating an attractive offering for people looking to create credit and pay off debt through home improvement projects.

Major Purchases With Upgrade Personal Loans

Making a major purchase is a necessary decision for many consumers. Upgrade Personal Loans offer the perfect solution to finance larger purchases. Customers get access to funds through a secure platform from anywhere in the world with flexible payment options and low-interest rates.

Upgrade’s loan offers several advantages that make it easier for customers to complete their big purchases without worrying about budgeting or overspending. Customers can choose between fixed-rate loans with predetermined monthly payments, adjustable-rate loans with fluctuating payments based on current market conditions, and secured loans with collateral required upfront. Upgrade’s online application process is easy. Applicants only need basic information such as name, address, and income details to be approved within minutes of applying.

The Upgrade experience includes helpful tools like debt consolidation, which allows customers to pay off multiple debts at once by combining them into one single payment instead of dealing with multiple bills each month. It makes it much easier for customers to keep track of their finances while helping them save time and money in the long run. Customers have 24/7 access to customer service representatives available for extra assistance.

Credit Score Impact Of Upgrade Personal Loans

An upgrade personal loan is a viable option when making major purchases. For example, John Doe is interested in buying a new car and takes out an upgrade personal loan to pay for it. Upgrading a personal loan can have a long-term impact on his credit score. Listed below are the activities that impact your credit score.

- Any late payments results in extra fees and stay on the borrower’s record for up to seven years.

- The debt-to-income ratio has been affected by getting the loan;

- Getting the loan increases exposure to risk due to potential interest rate fluctuations.

- More open accounts mean more chances for incorrect information or fraudulent activity.

The overall effect of upgrading personal loans on one’s credit score largely depends on how they are managed and paid off over time. Regularly checking your report helps keep track of any discrepancies while utilizing budgeting strategies such as setting aside money towards repayment helps guarantee timely payment of debts.

What are the Qualifying Criteria For Upgrade Personal Loans

The most basic aspects of upgrading personal loans include verifying creditworthiness by reviewing current credit scores and payment history on existing debts. Lenders require information about employment status, time at the job, annual salary, and other details around potential liabilities such as child support payments or alimony obligations. It is necessary to note that each lender will have different criteria when approving or denying applications. Knowledge of the overall qualifications provides insight into what works best for any given situation.

Other Factors To Consider Before Applying

Considering other factors beyond the credit score when upgrading personal loans is necessary. Applying for a loan has long-term financial implications, so careful accounting must be taken before deciding.

Potential borrowers must assess their current financial situation and determine if they can afford the monthly payments associated with an upgraded loan. Individuals must research any fees or penalties associated with early repayment to guarantee that taking on additional debt does not outweigh the benefits of refinancing. Consumers must consider any changes to terms and conditions when comparing multiple offers from different lenders.

Tips For Obtaining An Upgrade Personal Loan

There are a few tips that are helpful when it comes to obtaining an upgrade personal loan. Listed below are the tips for obtaining an upgraded personal loan.

- Researching – First and foremost, the lender must be researched to determine if they offer competitive interest rates and flexible repayment plans.

- Credit score update – Potential borrowers must guarantee their current credit score to guarantee access to the best terms available.

It’s necessary for individuals looking for an upgrade personal loan to review their budget carefully and create a plan for how the money will be spent. An emergency fund already established before getting a loan is strongly recommended if unforeseen events lead to financial hardship. Doing it ahead helps prevent unexpected expenses or overspending once the loan has been approved and funds become accessible.

What are the Common Mistakes To Avoid When Applying

The Common mistakes when applying for such type of loan include:

- Needing more information about the lender.

- Failing to provide sufficient documentation. Needs to be more accurate in the amount needed.

The common mistakes that must be avoided when applying for a loan are listed below.

- Not researching – Prospective borrowers must research multiple lenders and compare interest rates. Understanding their terms helps individuals make decisions before signing any contracts.

- Not estimating needed funds – It is necessary to accurately estimate the required funds, as getting too little or too much money leads to difficulties later on.

- Not preparing for necessary documents – Note that all relevant documents, such as proof of employment status and tax returns, must be provided. The lender rejects applications without the said documents.

What are Refinancing Options With Upgrade Personal Loans

Refinancing options with Upgrade Personal Loans are a great way to pay off debt and create credit. Many people are unaware of the benefits of refinancing, such as lower interest rates on their loans or more accessible payment plans. Understanding the benefits before taking advantage of them is necessary to guarantee they work best for an individual’s financial situation.

There are key things to note when it comes to personal loan refinancing.

- Shop for the best deal – different lenders have different terms and conditions. Compare the offers and find one that works best for you.

- Check your eligibility – Many lenders use factors like income level, credit score, employment history, etc., to decide if someone qualifies.

- Understand fees & penalties – Other lenders charge upfront or late penalties if payments are missed or made after the due date.

Upgrade Personal Loans allow individuals to refinance existing debts into new ones with beneficial terms and conditions. The process helps save money by reducing monthly payments, consolidating multiple debts into single payments, and potentially lowering interest rates. It is necessary to research all available options before making a final choice, as with any major money management decision.

Pros And Cons Of Upgrade Personal Loans

Upgrade personal loans provide an attractive refinancing option for people seeking to accomplish the task. To make decisions, one must understand the pros and cons of personal loans.

Pros

- Low interest – Upgrade personal loans are secured with collateral or assets from the borrower. It offers lower interest rates than unsecured loan options such as credit card bills or credit cards.

- Accessibility – They are accessible from various sources, including banks, online lenders, or peer-to-peer networks.

- Able to be consolidated – Upgrading is beneficial if you want to consolidate multiple payments into one single payment of a lower monthly amount, such as consolidating credit card bills.

Cons

- Collateral – Applying for an upgraded personal loan requires a form of security unavailable for everyone depending on your financial position and risk profile.

- Includes extra fees – It involves extra fees like origination fees or closing costs, which must be considered when evaluating if an upgrade personal loan is right for you, especially when compared to the cost of managing credit card bills.

Advantages and disadvantages are associated with upgrading personal loans, which must be evaluated before deciding to create credit and pay off debt. You can guarantee that finding a suitable solution brings you closer to achieving your long-term goals with careful research on all aspects of personal loans and understanding their implications for your finances.

Create Credit And Pay Off Debt With Upgrade Personal Loans

One advantage of Upgrade Personal Loans for creating credit is that their loan amounts range from one thousand dollars to fifty thousand dollars with fixed rates. It allows customers to borrow exactly the amount they need without risking overspending or taking a loan they cannot afford. Upgrade offers flexible repayment terms, which makes payments more manageable and less costly in the long run. There is no pre-payment penalty, so customers can pay off their loans early if desired.

One potential downside of using upgrades for credit creation and payment is that certain fees, such as origination fees, apply. Applicants must note that only people with good credit scores receive approval. People with average or bad credit still qualify depending on individual qualifications and circumstances. It must be noted that personal information must be provided when applying for a loan, including name, address, and social security number, which leads to identity theft unless handled securely.

Maximizing The Benefits Of Upgrade Personal Loans

Using Upgrade Personal Loans to create credit and pay off debt is highly beneficial if done strategically. Upgrading personal loans is an innovative option with advantages not found in traditional lending methods.

- Quick access – It allows individuals to access funds quickly while providing the opportunity to build their credit score. The process allows borrowers to set up monthly payments on time and in full over time, gradually building their credit scores.

- Approval – Upgraded personal loan helps people who have trouble getting approved for other types of financing due to poor credit history or lack of income.

- Flexibility – Upgrading personal loans provides flexibility regarding repayment terms and interest rates. It makes them easier to manage than traditional approaches.

- Competitive rates – They offer more competitive interest rates than most other forms of borrowing, making them attractive options for people looking to save money on debt repayments.

Personal loans are a great choice for financial freedom and increased control over their finances. Individuals maximize the benefits of upgrading personal loan products by utilizing the loans strategically and staying disciplined with budgeting and repayment plans.

Managing Your Upgrade Personal Loan Responsibly

Managing an upgrade personal loan responsibly is a smart financial decision in the long run. By understanding how credit works, borrowers can reduce their debt faster while avoiding future problems with potential lenders. It is necessary to consider all available options before making any decisions and take steps that minimize debt quickly.

Borrowers find ways to pay off debts sooner than expected by researching different loan management options. Budgeting helps guarantee payments are made on time and that bills remain manageable even during difficult financial times. It includes taking advantage of low-interest rates and utilizing direct deposit into accounts associated with the loan. Taking action early on by setting up adequate savings or emergency funds aids in paying off the loan more easily.

Staying informed about changing interest rates and other factors affecting repayment plans is necessary. Making regular payments while keeping track of progress toward eliminating debt helps guarantee timely repayment without increasing overall costs due to extra fees or penalties from missed payments over time. Through careful planning, responsible management of an upgrade personal loan provides advantages such as improved credit ratings, which open doors for new opportunities.

Conclusion

The Upgrade Personal Loan is an effective tool for creating credit and paying off debt. There are several benefits to getting an Upgrade Personal Loan that make it a worthwhile investment while the APR is high. People with a bad credit history can use the loan to improve their scores. Home renovation financing can be obtained quickly, allowing homeowners to upgrade their property without waiting for funds from other sources.

Managing financial responsibility with an Upgrade Personal Loan is necessary to maximize its potential benefits. Staying within budget when using the loan helps prevent overextending finances and falling into further debt. Payments on time help build credit while avoiding fees associated with late payments guarantees one does not pay more than necessary.

Understanding how an Upgrade Personal Loan works and utilizing it responsibly can create credit and pay off debt effectively. Homeowners have access to quick funding for home renovation projects, while people with little or no credit history can improve their scores over time through smart fiscal management. The key lies in assessing individual needs accurately and keeping track of all payments made towards the loan balance to reap maximum rewards from a useful product.

Frequently Asked Questions

What are the key factors that affect my credit score?

The key factors are payment history, amounts owed or credit utilization, length of credit history, new credit applications, and mix of credit types like credit cards, loans, and mortgages.

How can I improve my credit score if it’s low?

Strategies include paying bills on time, lowering debt, avoiding new applications, allowing time to pass, disputing errors, and practicing responsible credit use through managing a mix of account types.

What is the difference between secured and unsecured debt?

Secured debt is tied to an asset used as collateral like a mortgage or auto loan. Unsecured debt has no collateral like with credit cards, medical debt, or personal loans.

What strategies can I use to pay off high-interest credit card debt?

Strategies include transferring balances to a lower rate card, consolidating into a debt management plan or personal loan, attacking highest interest debt first, cutting expenses to increase payments, and negotiating lower rates.

How do balance transfers work, and are they a good option for debt consolidation?

Balance transfers move debt onto a new card with a promotional 0% rate for a limited time. They can temporarily save on interest but have fees. They work best for those who can pay off debt quickly.