The Pros and Cons of Consolidating Your Debt

Most Americans will need financial assistance at some point. It could be for buying a house, paying off medical bills, student loans, buying a car, or purchasing consumer goods with credit cards and store accounts.

While a credit line can provide benefits such as allowing you to purchase the items you need in affordable installments and improving credit scores, it can also negatively affect your finances.

You could end up with much more debt than you can pay with your paycheck. People feel frustrated and stressed when they are unable to find a solution.

Therefore, it is a question whether consolidating debt with personal loans is a good idea. This article will discuss debt consolidation loan and the pros & cons of Americans loan for debt consolidation.

What Is Debt Consolidation?

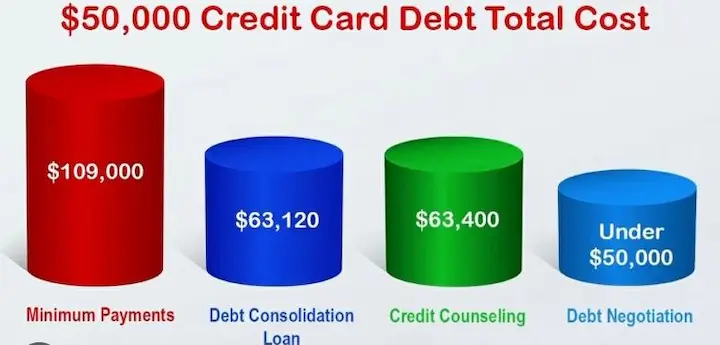

Debt consolidation combines multiple debts into a single payment, usually with a debt consolidation loan. There are different types of debt consolidation, including credit card debt consolidation and other methods. The debt consolidation process typically involves working with a debt consolidation company to negotiate a lower interest rate or a longer repayment term for your consolidated loan. The advantage of debt consolidation is that it may help to reduce the stress of managing multiple credit card bills and other debts. It can result in significant savings over time and help you manage your monthly payments more efficiently.

Consolidating your debt involves applying for a debt consolidation option like a personal loan from a bank to consolidate it. You can use the loan to pay off existing debts. Depending on the loan amount, you may combine multiple debts into one single payment. Clients with severe financial constraints will likely take this step to reduce their debt. Debt consolidation lenders offer various options, such as specialized debt consolidation loan, credit card consolidation, or student loan consolidation.

Consolidating Debt Is a Benefit

Consolidating debt with loans is the best way to get rid of debt. For more information, please see the following:

Convert Multiple Payments Into One

Consolidating debt can be a way to simplify your budget and form a solid consolidation plan. A monthly budget can be stressful if you have many accounts and bills.

Because you can see your money moving in different directions, depending on the severe situation, people may find that they don’t have enough money or that their salaries are insufficient to cover all their expenses. By creating a consolidation strategy and exploring common debt consolidation methods, you’re more likely to regain control of your financial situation.

It is a bad credit thing because creditors expect you to pay your account payments on time every month. Because there will only be one monthly payment, consolidating your debts can streamline your debt repayment process, unveiling the truth about debt consolidation.

A Personal loan can be beneficial depending on your loan’s repayment terms. It will have a lower monthly repayment rate, allowing you to spend more monthly money.

This loan is great for those with multiple credit card balances or store balances. You can pay them all off and only one creditor each month. Because you’re now focusing on one current debt, this makes it easy to feel calm.

Lower Interest Rates

Personal loans are typically more expensive than secured loan options, but they can improve your credit report. A personal loan online can help consolidate your debt, which is the truth about debt consolidation. Another benefit is the possibility of getting a lower interest rate.

Store accounts and credit cards have higher interest rates. You can reduce interest rates and save money by switching to one monthly payment.

It will allow you to focus on your debt repayments faster. Doing so is a great way to save money, keep your interest rates low, and focus on repaying your high-interest debt.

Increase Your Credit Score

Financial ruts can hurt your credit score and daily life. Your credit score will continue to be affected no matter how often you pay your debts off or miss them. Improving your financial habits can help you in the long run.

It all depends on how much of your debt load you have compared to your income. Credit bureaus will examine your credit history and how much credit you have used and conduct a credit check.

Credit utilization ratio is major in your credit score evaluation. It can indicate to creditors that you are not relying on your lines of credit in a way that is beneficial for you. As you age, your credit rating will improve if you apply for a loan to pay off all your debts. Credit utilization is low, which ultimately increases your credit score. Considering options like credit unions can also help improve your credit score.

Debt Consolidating Can Have Negative Effects

Although the application process for debt consolidation can be straightforward, it might not always be the best solution for everyone. It’s important to weigh the pros and cons and consider alternatives, such as debt settlement companies, before making the final decision.

Although there are many benefits to only one loan, it is important to consider all the possible drawbacks before you submit your loan application.

It Doesn’t Solve Your Debt Problem

Consolidating your debt can help you repay your debts and make monthly payments. However, it will not solve your problem. A balance transfer credit card or a debt management plan might be useful options to consider in this period of time.

This loan will help you get out of debt. Examining how you use the money and the mistakes you made in the past is important. You can ask yourself these questions:

- Do you rely on credit cards to make ends meet?

- Do you want a lifestyle that you can afford?

- Do you struggle to stick to your budget? Don’t know where to save money, or is your salary too low to meet your needs?

Understanding why you’re in this situation will help you make a better financial decision for the future, whether it’s considering loan terms or a debt management plan to tackle unmanageable debt.

Additional Charges May Apply

Consolidating loans can offer lower interest rates but higher costs. These fees can include closing costs, balance transfer fees, annual fees, protection plans, and other costs. It is also essential to be aware of the consequences of late payments.

Before applying online for a loan, it is crucial to do your research. You can use a personal loan calculator to estimate the cost. It’s also essential to consider the loan’s time payments, promotional period, and minimum payment.

You will be able to see what you are getting into. You want to avoid accepting a single loan offer and have a worse financial situation. Consider the type of loan you’re looking for and explore debt relief programs if necessary.

Higher Interest Rates

Lower interest rates may be possible. However, things can turn differently depending on your credit score and current interest rates. You could pay a higher interest rate if you apply for a personal loan.

It happens for many reasons, depending on the creditor’s guidelines. With a high outstanding debt or high monthly debt payment, lenders may view you as a riskier borrower. However, your credit score may be poor.

Lenders will always verify that you are not a high-risk or low-risk borrower. If they discover you have a poor payment history, they will increase your interest rate and possibly adjust your monthly loan payment.

It is worth asking yourself if paying a higher interest rate but only one payment for 12 months or several years or if you would prefer to find a way to repay your debt that doesn’t require you to take on more debt or pay more interest.

Does Consolidating Your Debt a Good Idea?

Debt Consolidation can help reduce anxiety and stress related to finances. It makes life easier and helps you see the bigger picture. It can also encourage control and a sense of control.

Consolidating debt should not make you worse off. It might not be beneficial if you don’t do enough research and get to know your financial situation. Do your homework and find the best personal loan for you before you make a request.

Frequently Asked Questions

What is debt consolidation, and how does it work as a financial strategy?

Debt consolidation combines multiple debts into one overall payment via a consolidation loan or balance transfer to save on interest and simplify finances.

What are the potential advantages and disadvantages of pursuing debt consolidation for my financial situation?

Benefits include lower interest rates, simplified payments, and potential credit score improvement. Drawbacks can include fees, eligibility issues, and repayment term length.

How can I determine if debt consolidation is the right choice for managing my debts?

Review your total balances, interest rates, monthly payments, credit scores, and new loan terms to calculate interest/fee savings and assess if it is beneficial.

Are there different methods or approaches to debt consolidation, and which one is best for me?

Balance transfer cards, personal loans, and debt management plans can consolidate debt. Compare rates, fees, eligibility, and impact to choose the best option.

What are some common misconceptions or pitfalls to avoid when considering debt consolidation as a solution?

Consolidation won’t erase debt and requires discipline in repayment. Avoid charging more after consolidating and consolidating federal student loans.